Dividend Irrelevance Theory

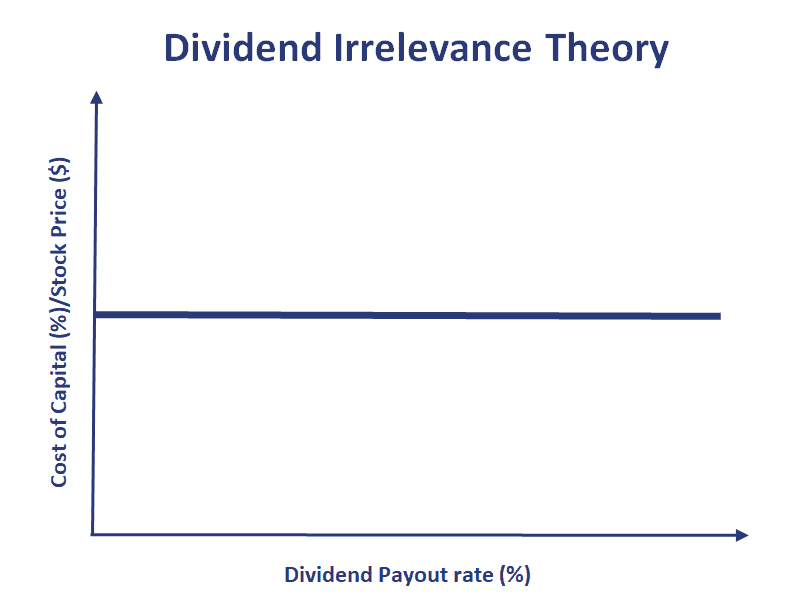

The Dividend Irrelevance Theory argues that the dividend policy of a company is completely irrelevant. The theory was proposed by Merton Miller and Franco Modigliani (MM) in 1961. In particular, MM argue that the dividend policy does not have an influence on the stock’s price or its cost of capital.

On this page, we discuss why Miller and Modigliani argue that the dividend policy does not matter. We also discuss the concept of homemade dividends, which is actually the main argument that underpins MM’s dividend irrelevance proposition.

Dividend irrelevance proposition

In a perfect world with no taxes, no brokerage costs, and infinitely divisible shares, the dividend irrelevance theory will hold. That’s because a stockholder who is unhappy with the dividend payout policy can create create homemade dividends. That is, if the investor is unhappy with the amount of dividends, then he or she can just buy or sell shares in the company.

Suppose the stockholder is of the opinion that the dividend is too big. In that case, the stockholder can reinvest part of the dividend by buying additional shares in the company. Similarly, if the investor thinks the dividend is too small, the stockholder can sell some of the shares he or she owns. In both cases, the value of the investment in the company and the cash in hand will be exactly the same. Thus, the amount of dividends does not matter.

Note that Miller and Modigliani’s dividend irrelevance proposition apply to the company’s total payout policy. This also includes share repurchases and other ways in which the company distributes the company’s net income to shareholders.

Arguments against the Dividend Irrelevance theory

Shortly after MM published their theory, Myron Gordon and John Lintner proposed an alternative theory called the bird-in-hand theory or dividend relevance theory that argues that investors prefer companies that pay out high dividends. That’s because a dividend in hand is more certain than the potential benefits of earnings that are reinvested by the company.

Summary

We discussed the dividend irrelevance proposition proposed by MM. It assumes a perfect world in which there are no taxes, transaction costs, and shares are infinitely divisible.