Dornbusch overshooting model

The Dornbusch overshooting model is a monetary model for exchange rate determination. The model was proposed by Rudi Dornbusch in 1976. The main idea behind the overshooting model is that the exchange rate will overshoot in the short run, and then move to the long-run new equilibrium. The model was proposed to solve the forward discount puzzle as well as the observed high levels of exchange rate volatility.

On this page, we first discuss the forward premium anomaly and then turn to the Dornbusch overshooting model.

Forward discount puzzle

The forward discount puzzle refers to the empirical observation that currencies with higher interest rates than other countries have appreciating currencies. This goes again the uncovered interest rate parity, which argues that these countries’ currencies should depreciate.

Dornbusch overshooting model assumptions

The Dornbusch exchange rate model holds under the following set of assumptions:

- a small open economy

- Exchange rates are flexible, that is, no capital controls or fixed exchange rates

- Sticky prices in the goods market (key assumption)

- Rational expectations

Dornbusch overshooting model definition

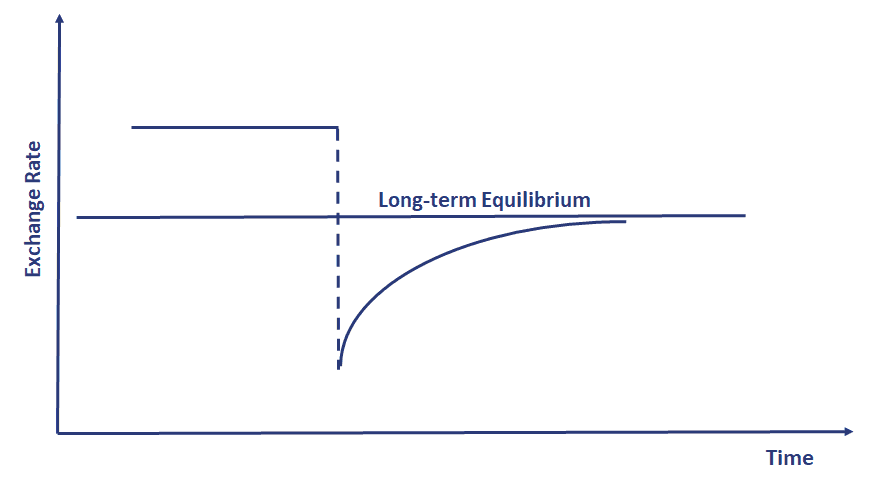

According to Dornbusch’s model, when a there is a change to a country’s monetary policy (e.g. and interest rate decrease), then markets will adjust to the new equilibrium. Because prices are sticky however, a new short-run equilibrium will be reached first financial markets. This equilibrium, however, is based on the old goods prices that are sticky. As the goods’ prices adjust, the exchange rate will change again. Hence, exchange rates initially overshoot by too much initially because they are still based on the old goods prices.

As the goods market adjusts, the exchange rate will adjust as well. It is only then that both the exchange rate and the goods market arrive at the long-run equilibrium. Clearly, this creates excess volatility. The exchange rate changed by too much initially and needs to correct to reflect the changes in the goods markets which it did not take into account initially.

Another implication of the Dornbusch overshooting model is that a currency can appreciate even if the interest rate of the country was lowered. That’s because the currency did indeed depreciate first, but by too much. Thus, the exchange rate then has to adjust to the long-run equilibrium which results in an appreciation. This may explain the forward discount puzzle described earlier.

Summary

We discussed the Dornbusch overshooting model. This elegant model explains the observed excess volatility and the forward discount puzzle.