Variance Swap

A Variance swap its payoff is based on variance. They are referred to as swaps because these contracts have two counterparties, one making a fixed payment and the other making a variable payment:

- The fixed payment is typically based on implied variance over the period and is known at the initiation of the swap. This is referred to as the variance strike (K).

- The variable payment is unknown at swap initiation and is only known at swap maturity. It is the actual variance of the underlying asset over the life of the swap and is referred to as realized variance.

On this page, we discuss how variance swaps work, how the settlement amount can be determined and finally how we can value variance swaps mark to market. We also implement a numerical example using Excel. The spreadsheet is available for download at the bottom of the page.

Variance swap definition

As we discussed in the introduction, there are two parties to a variance swap. The party receiving the variable payment (the purchaser) will gain on the contract when the realised variance is greater than the implied variance and will lose when the realised variance is less than the implied variance. Such a swap can, therefore, be viewed as a pure play on whether realised variance will be higher or lower than expected variance (implied variance) over the tenor of the swap.

There is no exchange of notional principal at the initiation of the swap. The swap also has no interim settlement periods. With such a swap, there is a single payment at the expiration of the swap based on the difference between actual and implied variance over the life of the swap:

where Nvar is the notional variance. The value of a swap is zero at initiation because implied volatility is the best ex ante estimate of realised volatility.

If, at expiration, realised volatility:

- is higher than the strike, the buyer of the swap makes a profit

- is lower than the strike, the seller of the swap makes a profit

Realised variance is calculated by taking the natural log of the daily price relatives, the closing price on day t, divided by the closing price on day t-1:

If we have N days of traded prices, we can compute N-1 price relatives R:

![$$ \textrm{daily variance} =[\frac{\sum_{i=1}^{N-1}R_i^2}{(N-1)}] $$](https://breakingdownfinance.com/wp-content/ql-cache/quicklatex.com-2a5170aa79238a10b21fbc00d1a009ea_l3.png "Rendered by QuickLaTeX.com")

annualized variance = daily variance x 252 days.

The notional amount of the swap can be expressed as either variance notional or vega notional. Variance notional represents the profit or loss per point difference between implied variance (strike²) and realised variance (sigma²). Variance notional can therefore be thought of as a multiplier that turns the point difference between sigma² and K² into a monetary amount:

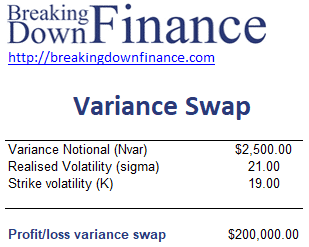

Variance swap example

The following table illustrates how we can calculate the profit or loss on a swap at settlement of the swap. The spreadsheet can be downloaded below.

Convexity

Because the payoffs on a variance swap are based on variance, while the strike price is expressed in terms of volatility, the payoffs of the swap are convex with respect to volatility. Compared to a volatility swap with payoffs that are linear with respect volatility:

- When realised volatility is below the strike, the losses on the variance swap are smaller than the losses on the volatility derivative

- When realised volatility is above the strike, the gains on the variance swap are greater than the gains on the volatility derivative.

In other words, the payoffs are increasing at an increasing rate when volatility rises and decreasing at a decreasing rate when volatility falls.

Summary

We discussed the basics behind variance swaps. We discuss how to mark to market these swaps separately.

Download the Excel spreadsheet

Want to have an implementation in Excel? Download the Excel file: Variance Swap example